Nebraska Delayed Deposit Services Bond: A Comprehensive Guide

This guide provides information for insurance agents to help their customers obtain Nebraska Delayed Deposit Services Bonds

At a Glance:

- Lowest Cost: $500 per year or $50 per month based on the applicant’s credit

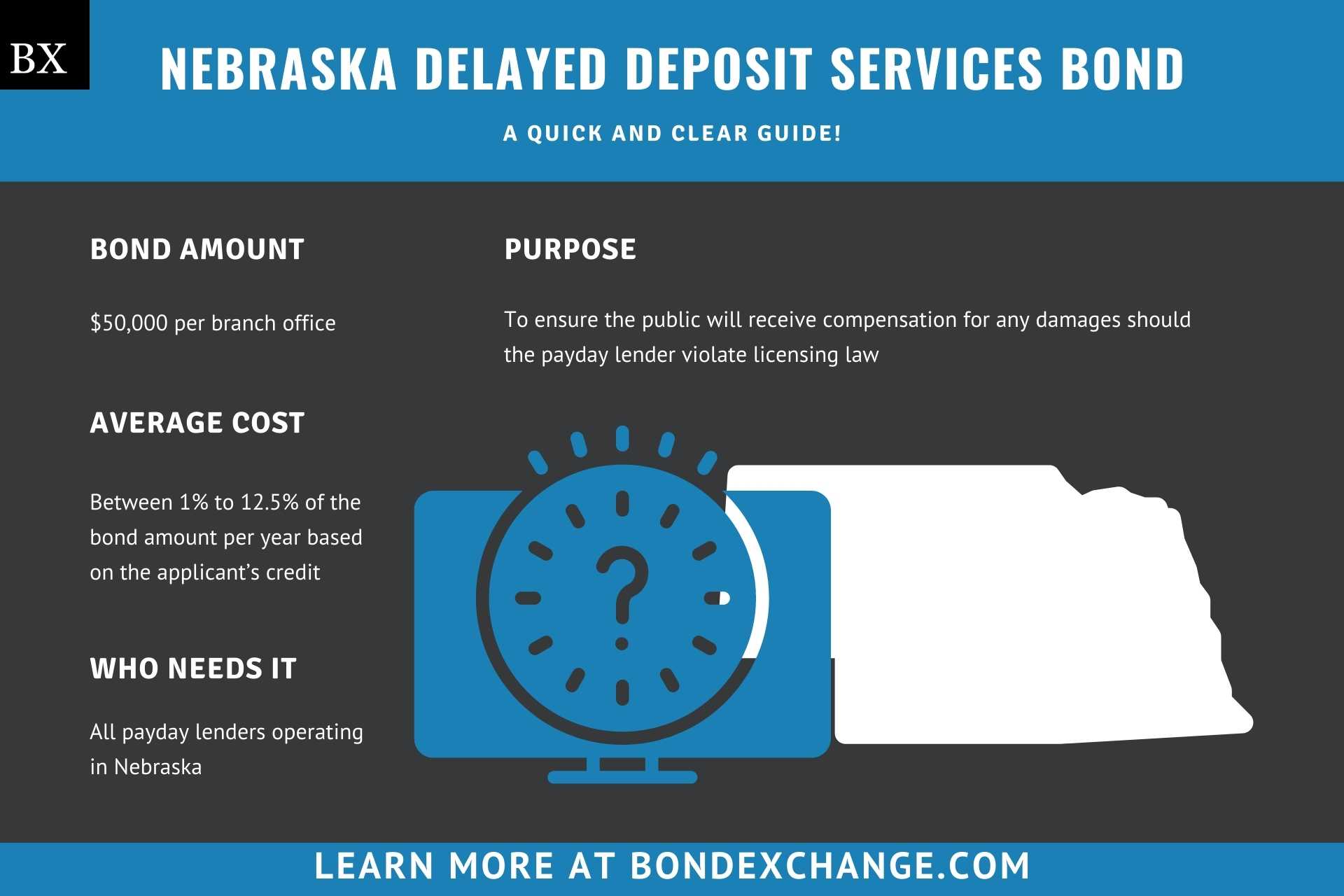

- Bond Amount: $50,000 per branch office

- Who Needs it: All payday lenders operating in Nebraska

- Purpose: To ensure the public will receive compensation for any damages should the payday lender violate licensing law

- Who Regulates Payday Lenders in Nebraska: The Nebraska Department of Banking and Finance

Background

Nebraska statute 45-904 requires all payday lenders operating in the state to obtain a license with the Department of Banking and Finance. The Nebraska legislature enacted the licensing laws and regulations to ensure that payday lenders engage in ethical business practices. In order to provide financial security for the enforcement of the licensing law, payday lenders must purchase and maintain a $50,000 surety bond (per branch office) to be eligible for licensure.

What is the Purpose of the Nebraska Delayed Deposit Services Bond?

Nebraska requires payday lenders to purchase a surety bond as part of the application process to obtain a business license. The bond ensures that the public will receive compensation for financial harm if the payday lender fails to comply with the regulations set forth in the Nebraska Delayed Deposit Services Licensing Act. Specifically, the bond protects the public in the event the payday lender engages in any acts of fraud or breaches any contracts made with consumers. In short, the bond is a type of insurance that protects the public if the payday lender breaks licensing laws.

How Can an Insurance Agent Obtain a Nebraska Delayed Deposit Services Bond?

BondExchange makes obtaining a Nebraska Delayed Deposit Services Bond easy. Simply login to your account and use our keyword search to find the “delayed” bond in our database. Don’t have a login? Gain access now and let us help you satisfy your customers’ needs. Our friendly underwriting staff is available by phone (800) 438-1162, email or chat from 7:30 AM to 7:00 PM EST to assist you.

At BondExchange, our 40 years of experience, leading technology, and access to markets ensures that we have the knowledge and resources to provide your clients with fast and friendly service whether obtaining quotes or issuing bonds.

Not an agent? Then let us pair you with one!

![]()

Click the above image to find a BX Agent near you

Is a Credit Check Required for the Nebraska Delayed Deposit Services Bond?

Surety companies will run a credit check on the owners of the payday lending company to determine eligibility and pricing for the Nebraska Delayed Deposit Services bond. Owners with excellent credit and work experience can expect to receive the best rates. Owners with poor credit may be declined by some surety companies or pay higher rates. The credit check is a “soft hit”, meaning that the credit check will not affect the owner’s credit.

How Much Does the Nebraska Delayed Deposit Services Bond Cost?

The Nebraska Delayed Deposit Services Bond can cost anywhere between 1% to 12.5% of the bond amount per year. Insurance companies determine the rate based on a number of factors including your customer’s credit score and experience. The chart below offers a quick reference for the approximate bond cost on a $50,000 bond requirement.

$50,000 Delayed Deposit Services Bond Cost

Table 1.2

| Credit Score | Bond Cost (1 year) | Bond Cost (1 month) |

|---|---|---|

| 720+ | $500 | $50 |

| 680 – 719 | $750 | $75 |

| 650 – 679 | $1,000 | $100 |

| 600 – 649 | $2,000 | $200 |

| 550 – 599 | $3,750 | $375 |

| 500 – 549 | $6,250 | $625 |

Who is Required to Obtain a License?

Nebraska statute 45-902 requires all business entities who perform one or more of the following services to obtain a Delayed Deposit Services License.

- Accepts a check dated subsequent to the date it was written

- Accepts a check dated on the date it was written and holds the check for a period of days prior to deposit or presentment pursuant to an agreement with or any representation made to the maker of the check, whether express or implied

BondExchange now offers monthly pay-as-you-go subscriptions for surety bonds. Your customers are able to purchase their bonds on a monthly basis and cancel them anytime. Learn more here.

How do Payday Lenders Apply For a License in Nebraska?

Payday lenders in Nebraska must navigate several steps to secure their license. Below are the general guidelines, but applicants should refer to the NMLS’s application guidelines for details on the process.

License Period – The Nebraska Delayed Deposit Services License expires on May 1 of each year and must be renewed before the expiration date

Step 1 – Meet the Net Worth Requirements

Applicants for the Nebraska Delayed Deposit Services License must have a company net worth (assets – liabilities) of at least $25,000. Applicants must submit a financial statement verifying their net worth when submitting their license application.

Step 2 – Purchase a Surety Bond

Payday lenders must purchase and maintain a $50,000 surety bond for each licensed branch office

Step 3 – Request a NMLS Account

The Nebraska Delayed Deposit Services License application is submitted electronically through the Nationwide Multistate Licensing System (NMLS). To submit a license application, applicants must first request to obtain an NMLS account.

Step 4 – Complete the Application

All Nebraska Delayed Deposit Services License applications can be completed online through the NMLS. Applicants must complete the entire application, and submit the following items:

-

- Company financial statements indicating a net worth of at least $25,000

- The following company contacts:

- Primary

- Primary consumer complaint

- Exam Delivery

- Pre-Exam Contact

- Exam Billing

- Disclosure questions

- Company’s AML/BSA policy

- Company business plan containing the following information:

- Marketing strategies

- Products

- Target markets

- Fee schedule

- Operating structure

- Certificate of Good Standing

- Copy of the payday lending contract/agreement

- Company formation documents

- Management chart detailing the company’s hierarchy

- Organization chart detailing the company’s ownership structure

- Security plan company will implement to ensure the safety and security of consumer records

- Biographical questionnaire for each company owner/officer

- Individual financial statements for each company owner/officer

Payday lenders must pay a $500 application fee, plus a $36.25 background check fee (per person), when submitting their license application.

How Do Nebraska Payday Lenders Renew Their License?

Payday lenders can renew their license online through the NMLS. License holders need to simply login to their account to access their renewal application. The Nebraska Delayed Deposit Services License expires on May 1 of each year and must be renewed before the expiration date.

What Are the Insurance Requirements for the Nebraska Delayed Deposit Services License?

Nebraska does not require payday lenders to purchase any form of liability insurance as a prerequisite to obtaining a business license. Payday lenders must purchase and maintain a $50,000 surety bond for each licensed branch office.

How Do Nebraska Payday Lenders File Their Bond?

Payday lenders should submit the completed bond form, including the power of attorney, electronically through the NMLS. The surety bond requires signatures from both the surety company that issues the bond and a representative from the payday lending company. The surety company should include the following information on the bond form:

- Name and count(ies) of entity/individual(s) buying the bond

- Surety company’s name

- Bond amount

- Date the bond goes into effect

- Date the bond is signed

What Can Nebraska Payday Lenders Do to Avoid Claims Against Their Bond?

To avoid claims on their bond, payday lenders in Nebraska must follow all license regulations in the state, including some of the most important issues below that tend to cause claim

- Do not engage in any acts of fraud

- Do not breach any contracts made with consumers

What Other Insurance Products Can Agents Offer Payday Lenders in Nebraska?

Nebraska does not require payday lenders to purchase any form of liability insurance as a prerequisite to obtaining a business license. However, most reputable businesses will seek to obtain this insurance anyway. Bonds are our only business at BondExchange, so we do not issue liability insurance, but our agents often utilize brokers for this specific line of business. A list of brokers in this space can be found here.

How Can Insurance Agents Prospect for Nebraska Payday Lender Customers?

The NMLS conveniently provides a public database to search for active payday lenders in Nebraska. The database can be accessed here. Contact BondExchange for additional marketing resources. Agents can also leverage our print-mail relationships for discounted mailing services.