What is an ERISA Bond?

At a Glance:

- Lowest Cost: $116 for a 3-year term or $4 per month, based on the bond amount

- Bond Amount: Minimum of 10% of the total plan assets

- Who Needs It: Employee benefit plan trustees

- Purpose: To ensure that plan beneficiaries will receive compensation for financial harm should the fiduciary commit fraud or dishonest acts

- Who Regulates Employee Benefit Plan Fiduciaries: The United States Department of Labor, Employee Benefits Security Administration (“DOL”)

What is the Employee Retirement Income Security Act?

The Employee Retirement Income Security Act of 1974 (“ERISA”) is a federal law created to regulate retirement and health plans for the protection of plan participants.

The legislation requires plan administrators to appropriately disclose financial information regarding the retirement plan, establishes regulations surrounding the role of the fiduciary, and provides plan participants with rights of recovery should they suffer harm due to the malfeasance or negligence of the plan administrator.

In order to provide financial security for the regulations set forth by the Department of Labor, fiduciaries must purchase and maintain a surety bond known as an “ERISA Bond”.

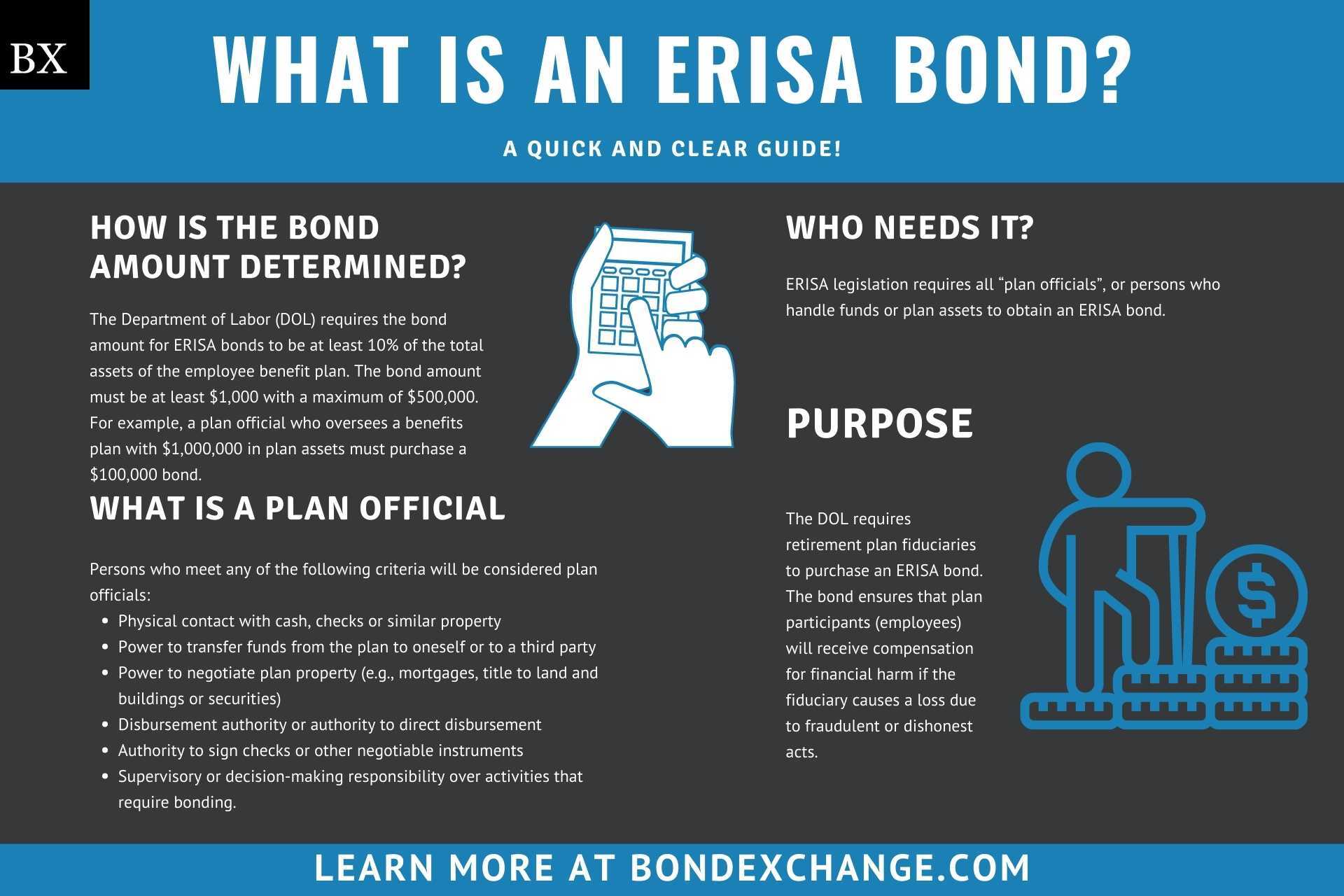

What is the Purpose of an ERISA Bond?

The DOL requires retirement plan fiduciaries to purchase an ERISA bond. The bond ensures that plan participants (employees) will receive compensation for financial harm if the fiduciary causes a loss due to fraudulent or dishonest acts.

In short, the bond is a type of surety bond that protects employees from unethical actions committed by plan fiduciaries.

How is the Bond Amount Determined?

The DOL requires the bond amount for ERISA bonds to be at least 10% of the total assets of the employee benefit plan. The bond amount must be at least $1,000 with a maximum of $500,000. For example, a plan official who oversees a benefits plan with $1,000,000 in plan assets must purchase a $100,000 bond.

Plans that include Non-Qualifying Assets (less common) will need to purchase a bond with an amount equal to the greater of (1) 10% of the total plan assets, (2) 100% of the valuation of the Non-Qualifying Assets, or (3) $1,000,000.

What Happens if the Plan Assets Increase to More than 10% of the Bond Amount?

If the plan assets accumulate or appreciate to an amount larger than 10% of the bond amount, the bond amount must be increased to stay in compliance with the DOL rule. However, many surety companies include a plan provision known as “inflation guard” that automatically increases the bond amount during the bond term to an amount that meets the DOL rule.

All BondExchange ERISA bonds contain this inflation guard provision for no additional charge, ensuring bond principals remain in compliance with DOL regulations.

BondExchange now offers monthly pay-as-you-go subscriptions for surety bonds. Your customers are able to purchase their bonds on a monthly basis and cancel them anytime. Learn more here.

What are the Underwriting Requirements for ERISA Bonds?

Most surety companies issue ERISA bonds “freely”, meaning no credit checks or financial review. However, underwriters will seek the following information when determining a fiduciary’s eligibility for a ERISA bond:

- Non-Qualifying Plan Assets – Does the plan include any non-qualifying plan assets such as real estate, limited partnerships, and non-participant loans?

- Number of Trustees – Are there more than 10 trustees associated with the plan?

- Multiple Employer Plan (“MEP”) Structure – Is the plan structured under a MEP?

If the answers to any of the above questions are “yes”, underwriters will ask for additional information about the plan and the plan trustees.

How Much Does an ERISA Bond Cost?

ERISA surety bonds cost between $116 to $425 for three years or $4 to $15 per month based on the bond amount needed.

ERISA Bond Cost

| Bond Amount | Bond Cost (3 Years)* | Bond Cost (1 month)* |

|---|---|---|

| $20,000 | $116 | $4 |

| $40,000 | $151 | $6 |

| $60,000 | $186 | $7 |

| $80,000 | $216 | $8 |

| $100,000 | $238 | $8 |

| $150,000 | $263 | $9 |

| $200,000 | $286 | $10 |

| $250,000 | $310 | $11 |

| $300,000 | $333 | $12 |

| $350,000 | $356 | $12 |

| $400,000 | $379 | $13 |

| $450,000 | $403 | $14 |

| $500,000 | $425 | $15 |

*Rates differ in the following States: AK, CA, & HI. Please contact BondExchange for rates in these states or for bond amounts not listed above.

How Can an Insurance Agent Obtain an ERISA Bond?

BondExchange makes obtaining an ERISA Bond easy. Simply login to your account and use our keyword search to find the “ERISA” bond in our database. Don’t have a login? Gain access now and let us help you satisfy your customers’ needs. Our friendly underwriting staff is available by phone (800) 438-1162, email or chat from 7:30 AM to 7:00 PM EST to assist you.

At BondExchange, our 40 years of experience, leading technology, and access to markets ensures that we have the knowledge and resources to provide your clients with fast and friendly service whether obtaining quotes or issuing bonds.

Not an agent? Then let us pair you with one!

![]()

Click the above image to find a BX Agent near you

Who Needs an ERISA Bond?

ERISA legislation requires all “plan officials”, or persons who handle funds or plan assets to obtain an ERISA bond. Persons who meet any of the following criteria will be considered plan officials:

- Physical contact with cash, checks or similar property

- Power to transfer funds from the plan to oneself or to a third party

- Power to negotiate plan property (e.g., mortgages, title to land and buildings or securities)

- Disbursement authority or authority to direct disbursement

- Authority to sign checks or other negotiable instruments

- Supervisory or decision-making responsibility over activities that require bonding.

Exemptions to this rule include:

- Benefits plans that only include the general assets of a union, employer, administrator, officers, and employees

- If the plan official is registered as a broker or a dealer

- A fiduciary shall be exempt from the bonding requirement if they meet any of the following criteria:

- Is a registered corporation

- Is authorized to exercise trust powers or conduct insurance business

- Maintains a combined capital and surplus of at least $1,000,000

Do ERISA Bonds Cover Multiple Employer Plans?

Legislation passed in September 2019 allows for Multiple Employer Plans (“MEPs”) to file a single annual report and obtain a single bond in lieu of a bond for each individual plan. That said, the bond amount will need to reflect the total combined assets of all plans covered under the bond.

Most surety companies will require additional underwriting for MEPs due to the potential for a large number of plan trustees.

Do Plan Officials Need to Purchase Additional Insurance?

No, plan officials are only required to purchase and maintain an ERISA bond. Though not explicitly required, some plan officials will purchase fiduciary liability insurance, which covers a more broad array of fiduciary breaches than an ERISA Bond.

What Can Plan Officials Do to Avoid Claims Against an ERISA Bond?

To avoid claims on an ERISA Bond, plan officials must follow all regulations set forth by the Department of Labor, including some of the most important issues below that could cause claims:

- Do not commit any acts of fraud or dishonesty against the plan, including but not limited to:

- Larceny

- Theft

- Embezzlement

- Forgery

- Misappropriation

- Wrongful abstraction

- Wrongful conversion

- Willful misapplication

What Resources Can Agents Use to Better Understand ERISA Bonds?

Insurance agents are encouraged to view the Department of Labor’s Field Assistance Bulletin for additional Information on ERISA bonds. If you have additional questions, give us a call at (800) 438-1162 to talk to one of our expert underwriters.